The Permian faced pipeline shortages a few months ago. This all changed as millions of barrels of takeaway capacity came online. Producers had been unable to transport oil from the region and crude oil produced in the Permian was heavily discounted getting $10 less per barrel compared to oil price in Houston or Corpus Christi only a year ago. Drilled but uncompleted wells can quickly go online and boost producer and midstream revenues.

Sizing the gap between production and takeaway capacity

Permian Basin producers currently pump 4.72 million barrels a day while pipeline takeaway capacity is 6 million barrels a day and growing. The Permian is fully de-bottlenecked now. It is expected that oil production in the Permian Basin will increase around 1 million barrels yearly, to reach 8 million barrels a day in 2023.

The gap between daily oil production and pipeline capacity out of the Permian Basin has diminished the price difference of crude in WTI Midland and WTI Houston. The spread between Midland and Houston has gone from $10 a year ago to around $2.50. Some companies turned to railcars for transport paying between $6 and $8 our barrel but that will not be necessary anymore.

A timely improvement to better serve export opportunities

Producers benefit from the improved pipeline capacity encouraging production, just in time for the expected increase in exports to China. After a more than a year-long tariff war, China committed to add at least $52.4 billion in energy purchases over two years, up from $9.1 billion in 2017. However, tariffs remain on many products, including a 25% tariff on LNG. We remain hopeful that these will also be removed soon.

The additional oil produced in the United States will be exported. Light crude, such as the one being produced in the Permian, has a better quality than what local refineries need, given that they were built for cheap heavy oil. Hence, only a third or Permian oil currently being produced is sold nationally and the rest is sent overseas. We consider that the region is now well prepared to increase sales to China and other countries.

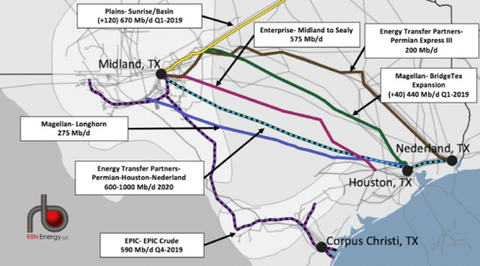

The Midstream actors and the scope of the new pipelines

Midstream companies have been adding capacity pushed by the booming production and increased interest in exporting US crude. The port of Corpus Christi alone exported 1.07mn b/d of crude oil in October surpassing Houston based exports. The Cactus 2 and the Epic line began service last August moving Permian crude to the Corpus Christi area with capacities of 670,00 b/d and 400,000 b/d respectively. The Epic line will soon add 600,000 b/d.

Source: RBN Energy

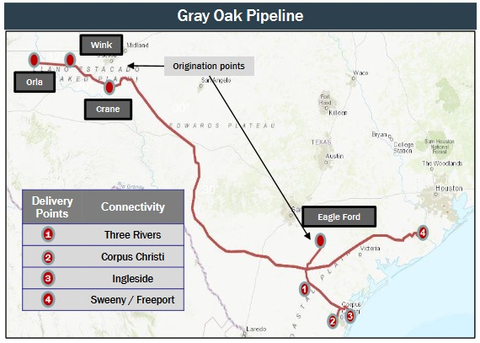

Similarly, Gray Oak started service in the fourth quarter of 2020 and will be 900,000 b/d by the end of the Q1 of 2020. The Sunrise pipeline extension added 120,000 b/d while the Seminole-Red added 200,000 b/d of takeaway capacity in 2019.

In the region, the Red Wolf Crude Connector with 120,000 b/d and the Gray Wolf Crude Connector with 120,000 b/d are in construction while it has been announced that the Jupiter pipeline with 1,000,000 b/d, the Voyager pipeline with 250,000 b/d, the Midland-to-Echo 3 pipeline system with 450,000 b/d and the Red River Pipeline with 85,000 will begin construction in 2020. Additionally, the Permian region will increase takeaway capacity with the Red Oak Pipeline wit 400,000 b/d, the Wink to Webster pipeline with 1,000,000 b/d, the Seahorse pipeline with 800,000 b/d which will start construction in 2021. These projects are planned to move crude oil throughout Texas and Louisiana to further alleviate regional constraints.

For Midstream companies, it will be very important to secure markets with producers now that the takeaway capacity is larger than current production. Spot rates will be comparatively low and times will be difficult for shale shippers while pipeline takeaway capacity is oversupplied. Pipeline operators will need to choose between lowering tariffs and sacrificing volumes during the incoming months, particularly when trying to renew long-term shipper contracts about to expire. Companies with well established infrastructure will have an advantage during these highly competitive times of strained profit margins. Still, some companies are forging ahead with pipeline expansions because of industry support.

What does it mean for you?

Market dynamics shifting in the Permian Basin

- Completion of long-expected pipelines.

- Entry of major players: Chevron, Exxon, Occidental Petroleum, and BP.

ExxonMobil’s rapid growth

- Permian output jumped 90% year-over-year, averaging 274,000 boe/d in 2Q2019.

- Plans to increase output to 1 million boe/d by 2024.

Pipeline developments

- Exxon joined Lotus and Plains All American to construct the Wink to Webster pipeline.

- Multiple projects may lead to future competition for pipeline space.

Market impact of majors

- Companies pursue large integrated projects that are less price sensitive.

- The shale industry has shifted to a scale game, favoring big players.

Impact on oilfield services

- The trend toward consolidation will pressure oilfield service companies.

Independent producers are relatively inexperienced with the complexities of exporting and new intermediaries might step into the market or acquisitions might continue. Smaller producers will need to cope these pressures applying strong capital discipline. US refineries are already buying all the light crude they can use from domestic suppliers. Most of the additional 4 million barrels per day of crude coming out of the Permian Basin over the next few years will have to be exported.

Employment continues to be high in the region, there is a shortage of skilled workforce for construction and operations. About 171,000 well paid jobs are supported by pipelines in Texas. The local economy benefits from pipelines. From 2014 to 2024, pipelines will contribute with about $2 billion in new state and local tax revenue literally keeping the economy pumping. It is estimated that pipelines in Texas will contribute $374 billion in total economic output between 2014 and 2024.

Regardless of where you are in the industry, if H2S is present in your volume, it is likely creating a value gap. Q2 Technologies’ Pro3®, Pro3® Nano, and ProM®, for crude, gas, and mercaptans, respectively, can chemically alter the H2S or mercaptans out of the equation for you. Contact us today to increase value wherever you are in the lifecycle of that hydrocarbon.